AKS Steel Expects An Increase In Average Selling Price

Posted: January 25, 2010 Filed under: earnings reports, Steel | Tags: AK Steel, AKS Leave a commentAK Steel (AKS) fourth quarter and annual earnings this morning. The outlook for the first quarter includes an expected increase in average selling price of 3-4%. This price hike appears consistent with a recent series of price hikes from AKS (as reported here on Inflation Watch).

AKS returned to profitability in the third quarter of last year and expects to remain profitable in this year’s first quarter despite shipments remaining flat with fourth quarter levels.

Full disclosure: author intends to purchase AKS today

Base Effects Add to the Bank of Canada’s Inflation Concerns

Posted: July 13, 2023 Filed under: Canada, Economy, Monetary Policy | Tags: Bank of Canada, base effects, FXC, Invesco CurrencyShares Canadian Dollar Trust, Monetary Policy, USD/CAD 1 CommentLast month, the Bank of Canada worried about inflation staying more persistent than expected and decided to release the pause button on rate hikes. In this month’s Monetary Policy Report, the Bank of Canada added “base effects” to its list of concerns about stubborn inflationary pressures (emphasis mine):

“While CPI inflation has come down largely as expected so far this year, the downward momentum has come more from lower energy prices, and less from easing underlying inflation. With the large price increases of last year out of the annual data, there will be less near-term downward momentum in CPI inflation. Moreover, with three-month rates of core inflation running around 3½-4% since last September, underlying price pressures appear to be more persistent than anticipated. This is reinforced by the Bank’s business surveys, which find businesses are still increasing their prices more frequently than normal.”

I have seen more and more references to base effects regarding U.S. inflation. In the previous two years, base effects could be used to dismiss inflation’s threat. This year, base effects from more challenging comparables are looming as the end of the tailwinds for disinflation (on a year-over-year basis). The timing is poor. As the Bank of Canada noted, underlying inflation has gone nowhere for almost a year. At this point, sticky inflationary pressures cloak more uncertainty around prior inflation expectations:

“In the July MPR projection, CPI inflation is forecast to hover around 3% for the next year before gradually declining to 2% in the middle of 2025. This is a slower return to target than was forecast in the January and April projections. Governing Council remains concerned that progress towards the 2% target could stall, jeopardizing the return to price stability.”

Surprisingly, markets took the news in stride. At the same time the U.S. stock market celebrated a pleasing report on U.S. June inflation, the Bank of Canada’s rate hike did not dampen spirits about the prospects for a more dovish Federal Reserve. Currency markets reacted as though the Fed might even be closer to rate cuts as losses in the US. dollar continued apace.

In fact, the market almost seemed to skip right over the Bank of Canada’s news. While majors like the euro and the British pound rallied all day against the U.S. dollar, the Canadian dollar enjoyed just brief intraday strength in the wake of the Bank of Canada’s decision to hike rates another 25 basis points. At the time of writing, USD/CAD is only just now returning to its low point following the rate hike (and looks stalled right at support).

On a daily basis, the Canadian dollar looks set to resume its momentum against the U.S. dollar IF USD/CAD breaks below yesterday’s low. Otherwise, a countertrend rebound could take USD/CAD right back to downtrending resistance at the 50-day moving average (DMA) (the red line below) as the next move.

I remain bearish on USD/CAD (bullish the Canadian dollar), and I expect rallies to continue to fail just as they have since September. The path downward on USD/CAD (upward for Invesco CurrencyShares Canadian Dollar Trust (FXC)) has been slow and choppy yet ever so slightly biased toward more relative strength for the Canadian dollar. The next major test comes with the Federal Reserve’s meeting later this month. More Fed hawkishness at that time could refresh the U.S. dollar against all majors for a spell.

Be careful out there!

Full disclosure: no positions

Did Alan Blinder Suggest the Fed Should Have Done Nothing About Inflation?

Posted: January 19, 2023 Filed under: Monetary Policy | Tags: Alan Blinder, Federal Reserve, Monetary Policy, PCE 6 CommentsThe Claim

Former Fed Governor and current Princeton Economics professor, Alan S. Blinder wrote an opinion piece in the Wall Street Journal that essentially implied the Federal Reserve need not have raised rates to battle inflation. In a piece with the click-worthy title “What if Inflation Suddenly Dropped and No One Noticed?“, Blinder makes the following claim:

“Was the rest of the stunning drop in inflation in 2022 due to the Fed’s interest-rate policy? Driving inflation down was certainly the central bank’s intent. But it defies credulity to think that interest-rate hikes that started only in March could have cut inflation appreciably by July. There is an argument that monetary policy works faster now than it used to—but not that fast.”

Blinder goes on to explain that relief from supply and energy shocks were the biggest drivers of plunging inflation. Going forward, he thinks that the current five month decline in inflation is “…still too short a time to declare victory,” but he gives no explanation as to why going forward further Fed rate hikes will matter for getting inflation down this last mile of the way. I would have expected Blinder to argue that the Fed has already over-corrected for inflation.

Chasing the Trend In Inflation

It is pretty well accepted that inflation peaked several months ago. However, when Blinder worries that “no one will notice” the drop in inflation, he is worried about the finer technical details of trends. He breaks out the difference between earlier and current inflation to show how the year-over-year rate blurs the story.

“…the CPI inflation rate over the past 12 months has been an alarming 7.1%. But the U.S. economy got there by averaging an appalling 10.6% annualized inflation rate over the first seven months and a mere 2.5% over the last five. The PCE price index tells a similar story, though a somewhat less dramatic one. The 5.5% inflation rate over the past 12 months came from a 7.8% rate over the first seven months followed by a 2.4% rate over the last five.”

Blinder acknowledges that using this more refined (I will call it less lagged) approach would have also warned the Fed much earlier about inflation in 2021. In fact, it was recent trends that made loud skeptics of the Fed’s reassurances about “transitory” inflation.

Regardless, there is little magic or revelation in this breakdown. Blinder is simply providing a more technical description of what happens when a metric that quantifies changes over time peaks: the earlier components of that measure are, on average, higher than the more current ones. The graph below of the PCE (personal consumption expenditures) excluding food and energy juxtaposes the monthly change (grey line and vertical axis on the left) in the PCE with the annual change (black line and vertical axis on the right) in the PCE.

Source: U.S. Bureau of Economic Analysis, Personal Consumption Expenditures Excluding Food and Energy (Chain-Type Price Index) [PCEPILFE], retrieved from FRED, Federal Reserve Bank of St. Louis, January 19, 2023.

Note how the pre-pandemic stability in the monthly change supported stability in the annual change of the PCE. The annual change started to rise once the monthly changes started to rise to higher levels post-pandemic. The annual change reached a new, higher stability after the monthly changes stopped rising. Now, the monthly changes are finally producing a higher frequency of much lower numbers. Thus, the annual change looks like it has finally peaked. Stare hard enough, and you can even see the early makings of a declining trend.

Blinder worries that no one may notice the sudden drop in inflation. However, I suspect plenty of people have noticed the decline. There is a healthy collection of Fed critics and related folks who think the Fed over-reached after its first rate hike last March or May who are twisting the numbers every possible way to make the case that the inflation problem died a few months ago and/or the Fed has taken interest rates far too high, too fast. Again, because inflation has apparently peaked, it is easy to fathom that more recent inflation pressures are milder than earlier inflation pressures.

Where Is the Policy Implication?

Blinder’s WSJ piece avoided giving direct advice on monetary policy. However, he gave more clues in an interview with Marketplace. At the very end of the discussion, Blinder essentially said that the Fed should stop now, but they cannot do so because market’s will prematurely ease:

“The Fed is in a very ticklish position. They can’t be as frank as I just was with you. I could say anything, and I don’t move markets. If Jay Powell sneezes, he moves markets. It is too early to declare victory over inflation, it’s only six months. And that’s what Jay Powell or any of the Fed people would say if you had them on the radio. But I say it’s six months. Six months is not a week, six months is not two months. This is not a trivial length of time. I think it might take a year of this or, say, another six months to convince the Fed to declare victory. They’re not about to declare victory yet.”

Note how his advice here directly contradicts his caution in the WSJ piece that the timeframe for the inflation decline is too short to support victory laps. No wonder monetary policy can be so confusing.

Moreover, the Fed has been very clear about the metric it uses for the 2% inflation target: a year-over-year change that is demonstrably sustainable. The Fed cannot declare victory because the target as previously defined still sits out in the future. To suddenly change the timeframe to inflation over the last X months would undermine Fed credibility even more than the retreat from the “transitory” episode.

Ironically, with the Fed already effectively programming itself to end rate hikes in March, Blinder’s technical examination could be nearly moot…at least without specific policy prescriptions.

Be careful out there!

Inflation Expectations and Inflationary Psychology

Posted: October 17, 2022 Filed under: Central bank, Economy | Tags: fed funds rate, Federal Reserve, inflation expectations, interest rate, Monetary Policy, Richard Corbin, S&P 500, SPY, University of Michigan surveys of consumers 2 CommentsThe Federal Reserve’s aggressive fight against inflation has savaged financial markets. Along the way, I have taken note of bouts of navel-gazing over inflation indicators. Many of us have little operating experience navigating inflation, so perhaps it is natural to get sidetracked staring at an indicator or two that confirms a desire to see an end to inflation or that confirms the persistence of inflation. Since the U.S. last had an inflation problem over 40 years ago, the data samples are quite small for making conclusions for today’s unique mix of ingredients. Yet, since the Fed has expressed fears about entrenched inflationary psychology, consumer expectations for inflation have entered the basket of metrics used for assessing the Fed’s every move.

For example, back in April, 2022, Richard Corbin, a research professor at the University of Michigan who has directed the consumer sentiment surveys since 1976, issued this ominous warning in describing “inflationary psychology”:

“There is a high probability that a self-perpetuating wage-price spiral will develop in the next few years. Households have already become less resistant to paying higher prices and firms have become less resistant to offering higher wages. Prices and wages will continue to spiral upward until the cumulative erosion in inflation-adjusted incomes causes the economy to collapse in recession……Although consumers have increasingly expected higher inflation, they have also expected a strong job market and rising wages, especially among consumers under age 45. In the year ahead, wage gains will continue to reduce resistance to rising prices among consumers, and the ability of firms to easily raise their selling prices will continue to reduce their resistance to increasing wages. Thus, the essential ingredients of a self-perpetuating wage-price spiral are now in place: rising inflation accompanied by rising wages.”

“Inflationary Psychology Has Set In. Dislodging It Won’t Be Easy” – Richard Corbin

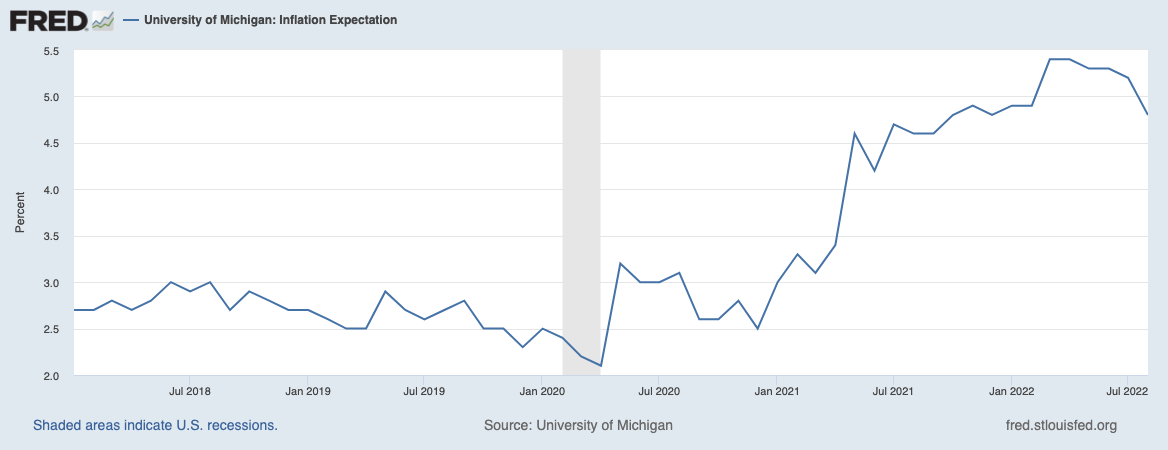

Note well that the University of Michigan’s U.S. consumer sentiment survey showed 1-year inflation expectations last peaked in March at 5.4%. There have been encouraging signs from the subsequent drift downward. However, hopes were dashed that these numbers could convince the Fed to pause after October’s 1-year expectation of 5.1% delivered a significant jump from September’s 4.7%. In other words, at best, expectations may be stabilizing at high levels, especially with core CPI surprising to the upside in September. Note, Corbin warned about over-extrapolating trends from wiggles in inflation numbers:

“Another critical characteristic of the earlier inflation era was frequent temporary reversals in inflation, only to be followed by new peaks. That same pattern should be expected in the months ahead.”

Surveys of Consumers, University of Michigan, University of Michigan: Inflation Expectation© [MICH], retrieved from FRED, Federal Reserve Bank of St. Louis, (Accessed on 10/16/2022, note the data are updated only through August per agreement)

For reference, the 5-year inflation expectations remain just above 2% which indicates consumers are still clinging to confidence that over the “long-term” inflation will return to the “before times”.

Federal Reserve Bank of St. Louis, 5-Year, 5-Year Forward Inflation Expectation Rate [T5YIFR], retrieved from FRED, Federal Reserve Bank of St. Louis, October 16, 2022.

Corbin wrote on the heels of the Fed’s first rate hike which was a mere 25 basis points. Corbin reacted with dismay and presciently argued:

“What was perhaps more surprising was that the quarter-point hike the Fed adopted in March was simply too small to signal an aggressive defense against rising inflation. Instead, it signaled the continuation of a strong labor market along with an inflation rate that would continue to rise.

Much more aggressive policy moves against inflation may arouse some controversy. Nonetheless, they are needed.”

Apparently, the Fed got the message and has been aggressively hiking starting with May’s rate hike!

If inflation expectations remain stubbornly elevated, then the time when the Fed is finally forced to take a pause could present a critical juncture of economic tension. In this scenario, I expect those who applaud the Fed’s pause will dismiss on-going high inflation expectations as transitory or even uninformed. Watch out if those expectations achieve new highs in the wake of a Fed pause.

The current controversy about aggressive policy demonstrates an instructive contrast with the last tightening cycle. What a difference pace can make! The S&P 500 (SPY) (red line with scale on the right) had little problem drifting higher while the Fed tightened with baby steps from 2016 to 2018. A sharp correction in late 2018 helped to convince the Fed to pause and then bring rates down. Market participants are still waiting for the Fed to care about the current market sell-off in the wake of higher rates.

Board of Governors of the Federal Reserve System (US), Federal Funds Effective Rate [FEDFUNDS], retrieved from FRED, Federal Reserve Bank of St. Louis; S&P Dow Jones Indices LLC, S&P 500 [SP500], retrieved from FRED, Federal Reserve Bank of St. Louis, October 17, 2022 (data available through September 1, 2022)

Be careful out there!

Full disclosure: short SPY put spread

Fed’s Daly: The Market Is Wrong About A Hump in 2023 Fed Rates

Posted: October 6, 2022 Filed under: commodities, Economy, iron ore, Monetary Policy, oil, Salaries | Tags: BHP, BHP Group, Fed Fund Futures, Federal Reserve, Mary Daly, Monetary Policy, real wages, UGA, United States Gasoline Fund 4 CommentsThe Federal Reserve board governors continue to stay on message, reminding the market over and over about its serious intention to fight inflation. San Francisco President Mary Daly has been particularly articulate on the Fed’s plan and what likely lies ahead. In an interview with Bloomberg Finance today, Daly informed financial markets that they are “wrong” to project what the interviewr called a “hump” in rate expectations. This hump is a peak sometime in 2023 with rate cuts to follow soon after. The current view from CME FedWatch has rates peaking from the February through June, 2023 meetings with a rate cut in July.

Daly’s steadfast perspective is important to remember every time the stock market rallies in anticipation of peak inflation and/or a “Fed pivot.” Indeed, Daly warned that the Fed needs to be prepared for inflation to be more persistent than expected. For context, Daly was one who was unwilling to predict peak inflation ahead of what turned out to be the “CPI shocker” that delivered a surprise of higher core inflation. Part of Daly’s persistence comes from what she and the Fed see as inflation’s greater potential for economic harm than the short-term consequences of normalizing monetary policy. Daly noted that over two years real wages have fallen 9%. She even shared an anecdote of a worker who told her about how he “loses” money when he goes to buy something with his earnings (an anecdote that speaks to nominal wages failing to keep up with nominal increases in prices).

Other interesting nuggets from the interview:

- Rates are probably now around the neutral rate, and the Fed needs to get slightly restrictive.

- The length of time rates stay neutral (or slightly restrictive) is more important than the specific level.

- 50% of today’s inflation is driven by demand (thus justifying the Fed’s desire to get slightly above neutral), 50% from supply.

- Daly refused to take the bait on the question of whether the Fed was purposely trying to induce a recession, trying to force losses on the stock market, or intent on hiking rates until something breaks.

- Daly insisted the Fed is forward-looking and recognizes lagging indicators of inflation.

- Daly pushed back on the notion the Fed needs to coordinate with global central banks. She insisted that the Fed must stick to its domestic dual mandate.

While the signs a few months ago were clear from commodity prices that the Fed’s actions were impacting inflation, the recent strength in oil threatens to rekindle inflation fears from the average person. For example, gas prices look like they are already done declining. The United States Gasoline Fund, LP (UGA) broke out today. UGA looks like it double-bottomed in September.

The recent downtrend in United States Gasoline Fund, LP (UGA) came to an end this week with a powerful breakout above 50 and 200DMA resistance.

Similarly, diversified commodities producer BHP Group (BHP) looks like it is holding a bottom in place since late last year.

BHP Group (BHP) has so far held its lows from a year ago. While upside may be limited, BHP also looks like it is done going down for now.

If these bottoms are indicative of what is ahead, then any soft readings in the near-term inflation numbers could be, well, transitory… (tongue-in-cheek intended!)

Be careful out there!

Full disclosure: long BHP

Persistently Elevated, Unactionable Inflation

Posted: June 10, 2022 Filed under: CPI | Tags: Bonawyn Eison, CNBC, CPI, Fast Money, Federal Reserve, Lindsey Piegza 4 CommentsBonawyn Eison, CNBC Fast Money commentator, used the phrase “persistently elevated, unactionable inflation” to describe the current inflationary cycle. Ahead of the disappointing report on May inflation, Eison pushed back on the “peak inflation” narrative as part of an attempt to “reverse engineer” a reason to buy the stock market. While he framed the desperate gaze over the inflation horizon in stock market terms, his characterization is quite appropriate for today’s overall inflation problem. Inflation has been persistent thanks to a powerful convergence of massive monetary stimulus, equally potent fiscal stimulus, and a host of economic disruptions. In turn, inflation promises to remain elevated for quite some time. Perhaps most importantly, the tools for fighting inflation are small compared to the size and the near intractability of the problem. For the Federal Reserve in particular the path to fighting inflation is fraught with the economic perils of stagflation.

The lure of the “peak inflation” narrative has been strong since the report on March inflation. The appeal is natural because of the sense that over time all economic conditions revert to the mean (or the average). However, the rush to declare the end of today’s problem with inflation has been particularly meaningful because it occurs in the middle of a desperate, global desire to return to some form of the “normalcy” we (think) we enjoyed before the pandemic. To their credit, various Federal Reserve members tried to soft pedal the idea of peak inflation, including the San Francisco President back in late April. They have remained nearly uniform in their stated resolve to focus on fighting inflation. The path from 8.6% to anything close to the Fed’s comfort zone does not start with hoping for a peak in inflation.

That 8.6% is where the headline Consumer Price Index (CPI) hit in May. Inflation hurtled March’s 8.5% for a new high for this inflationary cycle. The “peak inflation” crowd might now think surely inflation cannot go any higher from here. Perhaps this hope works out this time, but it matters little in the face of persistent and elevated inflation. Moreover, on the same Fast Money episode featuring Eison’s commentary, Lindsey Piegza, chief economist at Stifel, made an excellent point about the lagging nature of the CPI. Piegza pointed out that the worst impacts of the Russian invasion of Ukraine and the COVID lockdowns in China have yet to hit the CPI. If so, CPI may not continue to increase, but inflation will remain high for quite some time.

The broad-based nature of the May CPI increases suggests that inflation will indeed remain far above the Fed’s comfort zone for quite some time. Both the month-over-month and, of course, year-over-year inflation numbers were elevated across major categories (numbers are monthly and then year-over-year):

- Food: 1.0% and 8.6%

- Energy: 3.9% and 34.6%

- All items less food and energy: 0.6% and 6.0%

- New vehicles: 1.0% and 12.6%

- Used cars: 1.8% and 16.0%

- Shelter: 0.6% and 5.5%

The persistent rise in shelter costs is particularly notable given the Fed’s sudden sense of urgency on normalizing monetary policy implicitly came from housing costs.

I see at least one lesson from these numbers: inflation will not peak until it peaks. In other words, there is little point in straining the eyes over the horizon seeking the end of this inflationary cycle. Whatever the specific numbers, inflation here in the U.S. and across many nations promises to be persistent and elevated and will frustrate the economic agent who try to act against it without causing other economic fallout.

Be careful out there!

Jim Bianco: “Arguably One of the Worst Forecasts In Fed History”

Posted: April 8, 2022 Filed under: Bond market, Monetary Policy | Tags: Federal Reserve, iShares 20+ Year Treasury Bond ETF, Jim Bianco, Monetary Policy, TLT Leave a commentI thought *I* was critical of the Fed waiting so long to start normalizing monetary policy! Jim Bianco, President of Bianco Research, LLC, took criticism of the now moribund “transitory inflation” narrative to a new extreme. In an interview with CNBC’s Fast Money, Bianco took the Fed to task for what he called “arguably one of the worst forecasts in Federal Reserve history.” As a result, the Fed finds itself stuck with an inappropriately loose monetary in the middle of a high price, supply-constrained economy. The Fed intends to dampen demand through higher borrowing costs and lower stock prices (the wealth effect). The historic gap between job openings and the number of unemployed gives the Fed plenty of room to hike rates (until something breaks).

Fast Money invited Bianco after noticing an extended twitter thread that also took the stock market to task for ignoring rate hike risks. Bianco noted the dichotomy between a bond market that understands the Fed is more focused on controlling prices than growth, and a stock market that keeps doing its best to ignore the prospects. Bianco’s charts show that “the carnage is epic” in the bond market: “This is not only the worst bond market in our career (total return) but might be the worst of our lifetime.” Meanwhile, Bianco insists that what is ahead will hurt all financial assets.

The Trade

In “The Market Breadth“, I specialize in market opportunities at the extremes of behavior. So hearing that the bond market is suffering historic losses actually intrigues me. I suspect that sometime in the middle of an aggressive tightening cycle, bonds will present a generational buying opportunity. I am not a student of bond markets, so I will have to rely on the technical signals from a proxy bond instrument like the iShares 20+ Year Treasury Bond ETF (TLT). The weekly chart below suggests that the opportunity zone on TLT sits somewhere between the 2013 lows (government shutdown drama) and the lows of the financial crisis. I assume the lows of 2018 will be an insufficient stopping point, but I will watch closely for a bounce at that level. On the way down, I have been fading TLT rallies with put options.

Be careful out there!

Full disclosure: no positions

Stronger demand drives the latest AK Steel price hike

Posted: May 24, 2011 Filed under: commodities, Steel | Tags: AK Steel, AKS Leave a commentThe pricers at AK Steel (AKS) are at it again. This time, the company announced price hikes for carbon steel products:

“Base prices will increase by $50 per ton for hot rolled and cold rolled carbon steel products, and by $60 per ton for coated carbon steel products.”

AKS is facing higher input costs for making steel. More importantly, the company is experiencing stronger demand for its carbon steel products.

AKS has remained essentially flat for 5 months

Source: stockcharts.com

Disclosure: author owns shares in AKS

Input costs drive more price increases at AK Steel

Posted: April 6, 2011 Filed under: commodities, energy, Steel | Tags: AK Steel, AKS Leave a commentWhat’s a debate about inflation without more price hikes from a steel company?

AK Steel (AKS) announced additional surcharges today based on “…reported prices for raw materials and energy used to manufacture the products.” This announcement is one more small reminder of how commodity price pressures begin pushing their way through the supply chain:

“AK Steel…has advised its customers that a $390 per ton surcharge will be added to invoices for electrical steel products shipped in May 2011.”

Disclosure: author owns shares in AKS

AK Steel wastes no time increasing prices again

Posted: February 20, 2011 Filed under: earnings reports, Steel | Tags: AK Steel, AKS Leave a commentWhen AK Steel (AKS) reported earnings for the latest quarter, the company made it clear that it would drive for more pricing power with its customers. True to form, AKS has already announced three separate price hikes in the past in less than three weeks:

February 1

“AK Steel Announces March 2011 Surcharges For Electrical And Stainless Steels”

AKS announces “…a $430 per ton surcharge will be added to invoices for electrical steel products shipped in March 2011.”

February 10

“AK Steel Announces Price Increase For Carbon Steel Products”

AKS announces it “…will increase current spot market base prices for all carbon flat-rolled steel products, effective immediately with new orders. Base prices for carbon flat-rolled products will increase by $50 per ton.”

February 18

“AK Steel Announces Stainless Steel Price Increase”

AKS announces “…it will increase base prices for all 200, 300 and 400 series flat rolled stainless steel products, effective with shipments on February 27, 2011….Base prices of automotive exhaust grades will increase by $.04 per pound. In addition to the base price increases, AK Steel will increase the price for its bright anneal finish extra by $.05 per pound.”

Disclosure: author is long AKS stock

Steel prices pushing through the economy

Posted: February 6, 2011 Filed under: commodities, iron ore, Steel | Tags: AK Steel, AKS Leave a commentTalk to any steel company, and you will quickly discover the impact of commodity inflation. Steel companies in general have struggled to keep up with the soaring prices of coking coal and iron ore. It seems it is only a matter of time before these price pressures begin to push their way into the rest of the economy.

For example, in its latest earnings report, AK Steel (AKS) announced its plans for achieving greater pricing power by passing on input prices more quickly to its customers. We have also chronicled many of AK Steel’s price increases over the past year.

In “Steel-Price Increases Creep Into Supply Chain“, The Wall Street Journal demonstrates how steel companies are responding to higher input costs by passing along these costs to their customers:

“Steelmakers have increased prices six times, for a total increase of 20% to 30%, since November on basic flat-rolled steel, used in everything from cars to toasters, to offset higher input costs of raw materials, such as iron ore and coal. Higher costs for steel, which are expected to continue well into this year, are hitting bottom lines of companies and prompting additional price increases.”

The general expectation seems to insist that these pricing pressures will not percolate into final end consumer prices. However, I believe this thinking is just the lingering aura of the deflationary mindset of the last recession, and it will fade as surely as commodity prices have soared.

Disclosure: Author owns shares in AK Steel

AK Steel increases prices on carbon steel products

Posted: November 30, 2010 Filed under: commodities, Steel | Tags: AK Steel, AKS Leave a commentAK Steel (AKS) is increasing prices yet again. Effective today and starting with new orders, AKS announced: “…it will increase current spot market base prices for all carbon flat-rolled steel products…Base prices for carbon flat-rolled products will increase by $40 per ton.” AKS explained the reason for this price hike as a “…response to increased demand for carbon steel products, as well as the need to recover higher costs for steelmaking inputs.”

Since July, 2010, AKS has increased prices at least 10 times: four increases for carbon steel products and six increases in surcharges for electrical and stainless steel.

Full disclosure: author owns shares in AKS

Steel companies squeezed by lower product prices and higher input costs

Posted: October 28, 2010 Filed under: earnings reports, iron ore, Steel | Tags: AK Steel, AKS, Arcelor Mittal, MT, Steel, U.S. Steel, X Leave a commentA common theme has connected the earnings reports of most steel companies: lower prices for many steel products and higher input costs. This margin squeeze has produced poor earnings, and steel companies are providing very cautious outlooks. While pricing for steel products varies – some strong, some weak – the increasing cost pressures are near universal. Inflation is very real for these companies.

Arcelor Mittal (MT), AK Steel (AKS), and U.S. Steel (X) all reported this week. I have included some quotes from their earnings report to provide some examples of the pressures that these companies face.

“In Q3 the business performed towards the lower end of our expectations against a background of seasonally lower volumes, weakening spot prices and higher costs. Our outlook for Q4 remains cautious as the expected higher input prices continue to work through the business and demand remains muted, though with some regional differences.”

“Sales were lower during the third quarter of 2010 as compared to the second quarter of 2010 due to seasonally lower volumes (-8%), partly offset by higher average steel selling prices (+4%).”

“Sales in the Stainless Steel segment were $1.4 billion for the three months ended September 30, 2010, a decrease of 12% as compared to $1.5 billion for the three months ended June 30, 2010. Sales declined primarily due to lower steel shipments (-8%) as discussed above and lower average steel selling prices (-5%) due to a weak market environment and pressure from imports.”

“The company said its average selling price for the third quarter of 2010 was $1,075 per ton, a 2% decrease from the $1,101 per-ton price in the second quarter of 2010, and approximately 8% higher than the $994 per-ton average price realized in the third quarter of 2009.”

“2010 Iron Ore Price Increase Impacts Third Quarter:

AK Steel said that it has agreed with two of its three primary iron ore suppliers that the requirements for the establishment of the annual benchmark price of iron ore for 2010 have been met. That 2010 benchmark is an increase of 98.65% over the 2009 benchmark, and is higher than the 65% increase the company had previously estimated for the first half and for its third quarter guidance. The third primary supplier of iron ore to the company has not acknowledged yet that an annual benchmark price has been established. Instead, that supplier continues to seek a price increase in excess of the 98.65% annual benchmark price. The company does not agree that this supplier has a right under the parties’ contract to charge based on other than an annual benchmark price and, for purposes of the iron ore purchased from this supplier, the company has used an estimated benchmark price increase of 98.65% in its third quarter financial results.”

“The company’s third quarter 2010 financial results reflect the year-to-date impact of the higher iron ore price, which increased the company’s third quarter operating loss by approximately $76.0 million, or $52 per ton.”

“AK Steel said it expects shipments of approximately 1,300,000 to 1,350,000 tons for the fourth quarter, with an average selling price per ton decrease of approximately 4% from the third quarter. While the company expects fourth-quarter maintenance costs to decrease by about $20 million from the third quarter, it nonetheless expects to incur an operating loss of approximately $80 per ton for the fourth quarter of 2010, largely due to the lower shipments and selling prices combined with continued high iron ore and other raw material costs.”

(Quotes transcribed and paraphrased)

“Results declined in 3rd quarter from 2nd from lower flat-rolled average prices, higher raw material costs in flat-rolled segment and European operations: decreased shipments and production volumes, decreased average realized prices, increased costs for facility repair and maintenance (higher activity, not input costs), and consumption of higher cost coal, coke and iron ore purchased to support earlier facility restarts. Decreased spot prices more than compensated for increased contract prices.”

“In 4th quarter, expect lower average realized prices, lower spot and contract.”

“Tubular operations had higher average prices for fifth quarter in a row. Decreased costs for steel substrate. Not expecting same price performance in 4th quarter but costs should continue down.”

Disclosure: author owns X and AKS

AK Steel increases prices to offset rising material costs

Posted: September 17, 2010 Filed under: iron ore, Steel | Tags: AK Steel, AKS 1 CommentYesterday, AK Steel (AKS) warned investors that earnings would be lower than expected partly due to increasing material costs (mainly iron ore). Today, AK Steel told its customers that prices will increase as part of an effort to recoup some of those rising material costs. These price hikes are also enabled by strong demand for stainless steel products.

AKS will raise prices for specialty flat-rolled stainless steel products by about 5% to 10%. These products include “…tensilized, bright annealed and special finishes, along with special mechanical requirements.”

Full disclosure: author owns shares of AKS

Higher raw material costs contribute to AK Steel earnings warning

Posted: September 16, 2010 Filed under: earnings reports, Steel | Tags: AK Steel, AKS 1 CommentAK Steel (AKS) reduced its earnings outlook, partially due to higher material costs:

“The company’s revised third quarter outlook primarily reflects costs associated with the acceleration of planned maintenance work at its Ashland (KY) blast furnace, as well as higher raw material and operating costs than were expected at the time of its previous guidance…

…The impact of these changes on the company’s original guidance for the third quarter would result in an operating loss of approximately $20 per ton for the third quarter of 2010. The company’s original guidance was for an operating profit of $15 per ton for the third quarter. Nearly half of the lower expected financial results for the third quarter are attributable to the acceleration of the Ashland blast furnace outage.”

AKS goes on to state that it is expecting that the 2010 global iron ore benchmark price will increase higher than the company’s previous expectations for a 65% year-over-year gain.

Full disclosure: author owns shares in AKS

More price increases from AK Steel

Posted: May 4, 2010 Filed under: commodities, Steel | Tags: AK Steel, AKS 1 CommentSteel stocks have taken a beating since last making 52-week highs at the beginning of April. For example, the Market Vectors Steel ETF, SLX, is down 12% over this time (see chart below). However, the price increases continue to roll out from steel companies like AK Steel (AKS).

Yesterday, AKS announced two price hikes:

“…it will increase base prices for all 200, 300 and 400 series flat rolled stainless steel products by 6% to 9%, depending upon the grade and product form, effective with shipments on May 30, 2010.” (AK Steel Announces Stainless Steel Price Increase)

“…a $435 per ton surcharge will be added to invoices for electrical steel products shipped in June 2010.” (AK Steel Announces June 2010 Surcharges For Electrical And Stainless Steels)

Steel stocks have tumbled over the past month

Full disclosure: Author owns AKS

AK Steel Increases Prices on Carbon Steel Products

Posted: April 9, 2010 Filed under: Steel | Tags: AK Steel, AKS Leave a commentAnother month, another price increase for AK Steel (AKS). Yesterday evening, AKS announced a $40/ton price hike on all carbon steel products. The company explained the reasons for the increase:

“…the price increase is in response to increased demand for carbon steel products, as well as the need to recover higher costs for steelmaking inputs.”

The recovery in the steel industry continues…

Canadian Average Housing Price Sets New Record

Posted: February 9, 2010 Filed under: bidding wars, Housing, Monetary Policy | Tags: bubble, Canada, housing prices Leave a commentIn “Housing Rebound in Canada Spurs Talk of a New Bubble” the WSJ paints a familiar picture of what can happen to an asset market when interest rates drop to extremely low levels. Although Canada never experienced a housing crash like that of the U.S., the Bank of Canada still dropped rates to near-zero to help support the domestic economy. Its efforts to support exports (primarily to the U.S.) have been thwarted for much of the past year given the sharp rise in the Canadian dollar.

Here are some highlights from the article that describe the frenetic pace of the current Canadian housing market:

- The average home price rose 23% from the trough in January, 2009, hitting a record according to one broad measure.

- Home-sales volumes are up 70% since January, 2009.

- Housing starts in December reached levels last seen October 2008 (no indication whether these stats were seasonally adjusted).

- “Household debt—largely mortgages—was 1.42 times disposable income during the second quarter of 2009, a record high.”

The response of the Bank of Canada speaks to the trap facing policymakers as they contemplate transitioning monetary away from extremely accomodative levels. The WSJ reports:

“…Canada’s central bankers appear reluctant to take any steps that would hurt the economy. In a Jan. 11 speech, a representative of the Bank of Canada said: ‘If the Bank were to raise interest rates to cool the housing market now…we would, in essence, be dousing the entire Canadian economy with cold water, just as it emerges from recession.'”

The Canadians avoided the worst of the recent global meltdown. Let’s hope they did not avoid the fire only to land in the frying pan.

Higher demand and higher costs drive more AK Steel Price Hikes

Posted: December 10, 2009 Filed under: Steel | Tags: AK Steel, AKS Leave a commentAK Steel (AKS) continues to roll out price increases. On December 8th, AKS announced price increases on carbon steel products:

“[AKS] said today that it will increase spot market prices for its carbon steel products by $30 per ton for all new orders accepted for shipment on January 1, 2010 and later. This price increase is in addition to a previously announced increase of $20 per ton for carbon hot rolled products, and $30 per ton for carbon cold rolled and coated products, which is also effective with January 1, 2010 shipments.

AK Steel said that the price increase is in response to increased demand for carbon steel products, as well as the need to recover higher costs for steelmaking inputs.”

AK Steel Continues to Increase Prices

Posted: November 4, 2009 Filed under: Steel | Tags: AK Steel, AKS Leave a commentAK Steel (AKS) has been increasing prices on its steel products since the beginning of summer (click here for a summary). The pricing for December delivery continues the trend:

“AK Steel has advised its customers that a $185 per ton surcharge will be added to invoices for electrical steel products shipped in December 2009…AK Steel’s surcharges are based on reported prices for raw materials and energy used to manufacture the products, with the October 2009 purchase cost used to determine the December 2009 surcharges.”